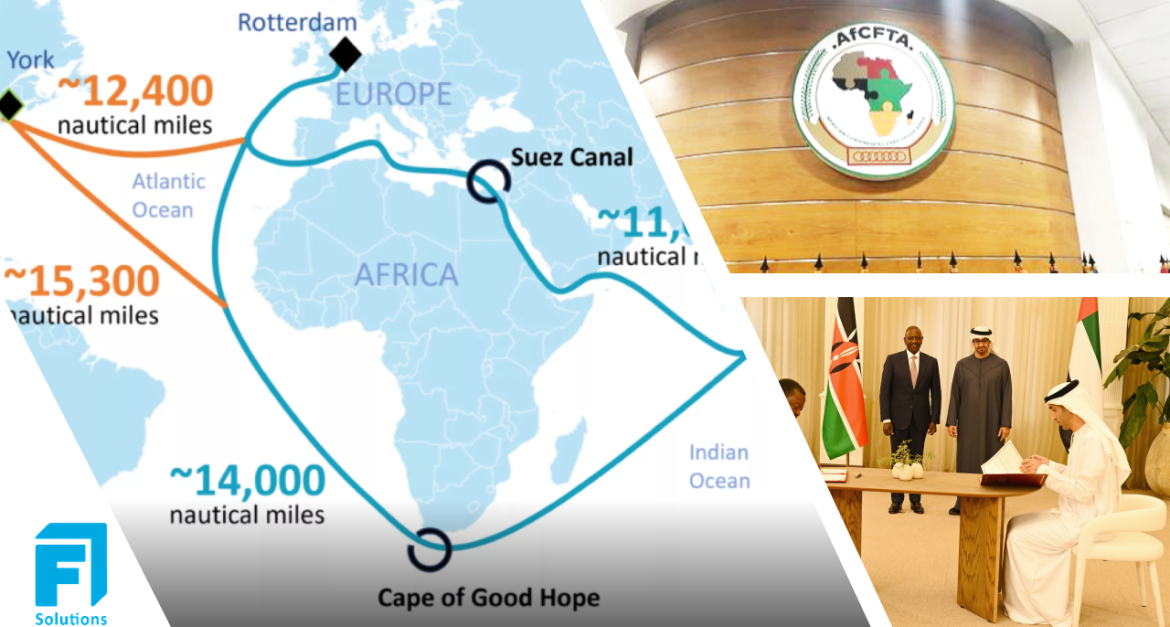

Red Sea Disruptions Push Ships South — and Force a Supply-Chain Recalculation

The Red Sea gave logistics teams another sleepless month. Renewed attacks kept carriers firmly committed to the Cape of Good Hope reroute — a detour that adds not just time, but layers of cost and complexity across supply chains.

By mid-November, congestion signals were flashing across southern and western ports. Cape Town and Walvis Bay reported vessel bunching; Tema saw rising dwell times; and Mombasa felt the knock-on effects as transhipment windows tightened. Freight rates on Asia–East Africa lanes held stubbornly high, with bunker surcharges and equipment repositioning eating into importers’ margins.

But beneath the operational noise lies the real story: planning cycles are being rewritten.

- Importers are increasing safety stock to avoid stockouts.

- Exporters are renegotiating delivery windows with clients.

- 3PLs are adjusting SOPs to protect SLAs, often absorbing some of the volatility to keep customers steady.

For businesses that rely on predictability, the Cape reroute isn’t just a headline — it’s a working capital issue. Longer transit times push cash conversion cycles outward, and the more sophisticated operators are now modeling 2026 with “long-route logistics” as a baseline, not an exception.

If November taught East Africa anything, it’s that agility is no longer a competitive edge — it’s the minimum viable posture.

AfCFTA’s Commercial Phase Expands — And Trade Starts Behaving Like a Real Market

Across Africa the industrial real-estate market is under pressure: grade-A warehouse occupancy has reached ~83 % in H1 2025, While global shipping wrestled with stormy seas, Africa quietly took a strategic step forward. More countries joined AfCFTA’s commercially operational phase under the Guided Trade Initiative, adding new product lines and lowering the practical barriers that once made cross-border trade feel like a marathon.

With Tanzania, Rwanda, Ghana, Senegal and others widening participation, the shifts are becoming visible in the data: more cross-border trucking, smoother customs handovers, and a growing appetite for regional consolidation hubs in Nairobi, Kigali, and Dar es Salaam.

This isn’t just a policy milestone — it’s a business model shift:

- Manufacturers are reassessing sourcing footprints to reduce import dependencies.

- Distributors are thinking in “regional SKU strategies” instead of country-by-country silos.

- 3PLs are positioning themselves to offer bonded storage + regional linehaul + last-mile as a single value proposition.

East Africa’s competitive advantage has always been location. But with AfCFTA gaining traction, the winning operators will be those who can provide predictable regional connectivity, not just local capacity.

The transition is slow, but it’s unmistakable: Africa’s trade is finally beginning to behave like a connected market, not a patchwork of 54 borders.

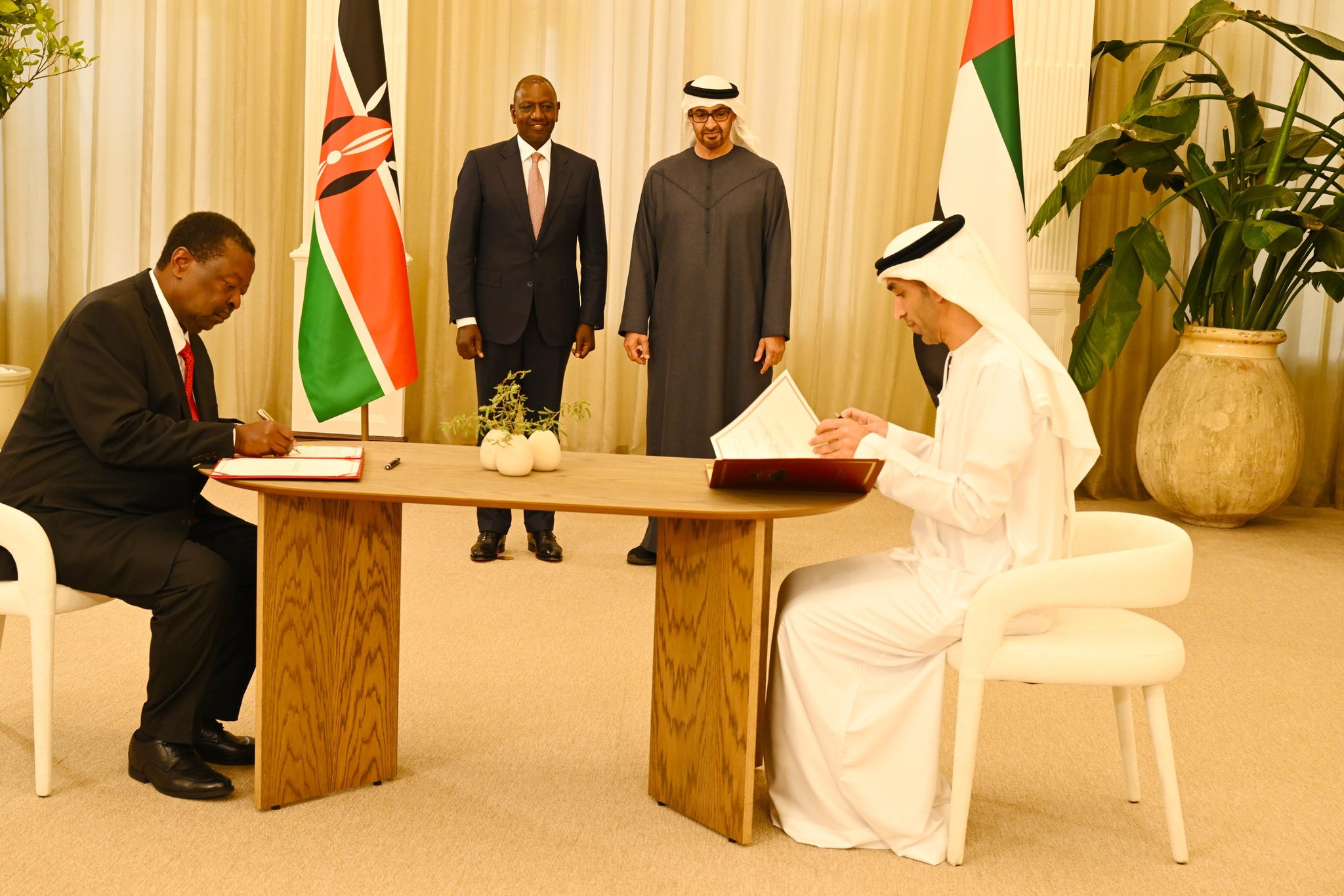

Kenya–UAE CEPA Advances — Strengthening a Corridor That Already Shapes Our Supply Chains

November also brought movement on the Kenya–UAE Comprehensive Economic Partnership Agreement, which entered its final refinement stage. It’s not flashy news, but for the logistics world it’s quietly significant.

The UAE is already one of Kenya’s largest trade partners — supplying fuel, machinery, plastics, electronics, and a huge share of the goods that pass through Mombasa, Jebel Ali and local distribution centres. A smoother CEPA could unlock:

- Shorter clearance and documentation cycles

- Lower or standardised tariffs on key import categories

- More predictable shipping schedules

- Increased demand for consolidation and fulfilment services

- Greater bilateral flows in re-exports and value-added goods

Put simply: CEPA could compress lead times and cost structures on one of Kenya’s most critical trade corridors.

For procurement teams, that means improved landed-cost stability.

For contract logistics providers, it means more Gulf-driven volumes, tighter SLAs, and stronger demand for modern warehousing.

For multinationals, it means the Mombasa–Dubai corridor becomes a more reliable anchor in their East & Horn of Africa supply-chain design.

In a month dominated by long detours and global uncertainty, CEPA was a reminder that some trade lanes are quietly becoming smoother — not rougher.