Strait of Hormuz Tensions Push Maritime Risk Premiums Higher

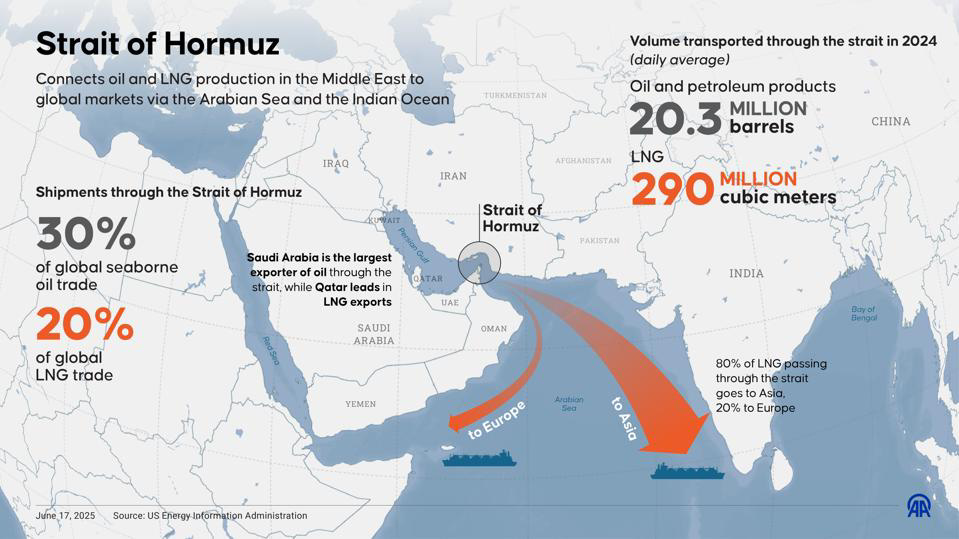

Global supply-chain uncertainty resurfaced in March as renewed security concerns around the Strait of Hormuz drove fresh volatility across shipping and energy markets.

Although geographically distant from East Africa, disruptions or instability around the Strait have immediate implications for regional logistics costs. A significant share of global oil shipments passes through the corridor, including Fuel from Kenya’s G-G arrangement with Gulf countries, making fuel pricing and maritime insurance markets highly sensitive to geopolitical tensions in the area.

For East African importers and logistics operators, the impact often arrives through rising bunker surcharges, higher war-risk insurance premiums, and growing freight-rate uncertainty.

Transporters operating inland are particularly exposed when fuel volatility intensifies. Even relatively small increases in diesel costs can quickly ripple across regional distribution pricing, affecting everything from FMCG deliveries to manufacturing supply chains.

The situation also highlights how interconnected modern logistics networks have become. A security incident thousands of kilometers away can quietly reshape freight planning, landed costs, and inventory decisions across East Africa within weeks.

For supply-chain teams already navigating tight margins and unpredictable transit schedules, geopolitical risk is increasingly becoming part of everyday operational planning rather than an occasional disruption.

Mombasa Port Efficiency Gains Help Reduce Cargo Delays

March brought encouraging signs from the Port of Mombasa, where ongoing operational improvements continued helping reduce cargo dwell times and improve overall cargo flow efficiency.

Closer coordination between port operators, customs authorities, and clearing stakeholders has gradually improved turnaround times, easing some of the congestion pressure that periodically affects regional cargo movement.

For importers and transporters, even modest improvements in cargo release timelines can significantly affect overall supply-chain performance. Faster port processing reduces truck waiting time, lowers demurrage exposure, and helps goods move more predictably into inland markets such as Uganda, Rwanda, and eastern DRC.

The challenge, however, is maintaining momentum as cargo volumes continue growing. Port efficiency is only as strong as the wider logistics chain supporting it. Delays at inland depots, border points, or transport scheduling stages can still undermine gains achieved at the port itself.

As East Africa’s trade volumes rise, the region’s logistics ecosystem is increasingly being judged not simply on infrastructure capacity, but on consistency and coordination across the entire cargo journey.

East Africa’s Cold Chain Investment Gap Draws Attention

March also renewed focus on one of the region’s most persistent logistics weaknesses: cold-chain infrastructure.

As demand for pharmaceutical distribution, fresh produce exports, and temperature-sensitive cargo continues rising, industry stakeholders increasingly warn that infrastructure investment is struggling to keep pace.

The challenge stretches across multiple areas — refrigerated transport availability, cold storage capacity, backup power reliability, and handling coordination between warehouses, airports, and distribution points.

For exporters and healthcare supply chains alike, cold-chain inconsistency carries serious commercial consequences. A few degrees of temperature variance during transport can affect shelf life, product quality, and customer confidence.

The investment opportunity, however, is equally significant. As East Africa’s consumer markets expand and export industries mature, demand for modern cold-chain capability is expected to grow substantially over the next several years.

For logistics providers, cold-chain performance is increasingly becoming a strategic differentiator rather than a niche service offering.