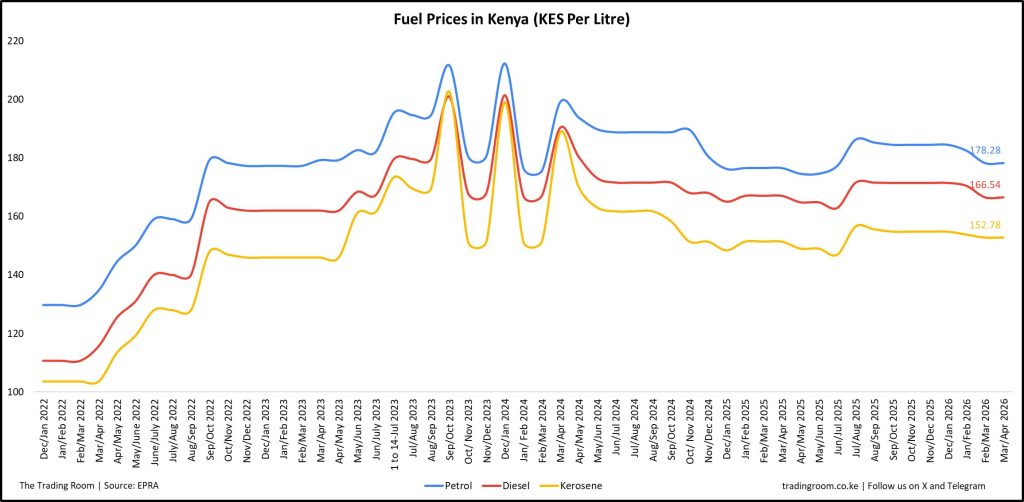

EPRA Fuel Price Hike Raises Pressure on Inland Transport Costs

Logistics operators across Kenya came under renewed pressure in April after EPRA announced another increase in fuel prices, pushing transport costs further upward across the supply chain.

Diesel prices — critical to long-haul and distribution transport — rose sharply, triggering concern among transporters and industry associations. The Kenya Transporters Association warned that continued fuel increases risked driving up freight costs across multiple sectors, particularly for inland cargo distribution.

For logistics providers, fuel remains one of the largest operating cost components. Even relatively modest price adjustments can materially affect route economics, fleet planning, and contract profitability.

The pressure is especially visible in regional transport operations where long-distance deliveries into Uganda, Rwanda, South Sudan, and DRC amplify fuel consumption exposure.

For customers, the effects often appear gradually through transport rate reviews, higher landed costs, or reduced pricing flexibility from suppliers attempting to protect margins.

The broader concern for the industry is predictability. Supply chains generally adapt better to high costs than to volatile costs. Frequent price swings make budgeting, procurement planning, and transport forecasting significantly more difficult across the logistics ecosystem.

Importers Continue Navigating Currency and Freight Volatility

Alongside fuel pressure, importers in April continued grappling with a difficult procurement environment shaped by currency fluctuations and unstable freight pricing.

Many businesses remain heavily exposed to dollar-denominated shipping and procurement costs, meaning exchange-rate movements continue directly affecting landed pricing and inventory budgets.

For procurement and supply-chain teams, the challenge is no longer simply securing cargo movement — it is managing uncertainty across multiple variables simultaneously: freight rates, fuel costs, exchange rates, and supplier lead times.

Some importers have responded by increasing order consolidation, adjusting inventory cycles, or renegotiating supply contracts to improve flexibility. Others are placing greater emphasis on regional sourcing strategies to reduce dependency on long-haul international supply chains.

The environment is also reinforcing the importance of supply-chain visibility and planning discipline. Companies with stronger forecasting capabilities and more integrated logistics coordination are generally better positioned to absorb market volatility without significant operational disruption.

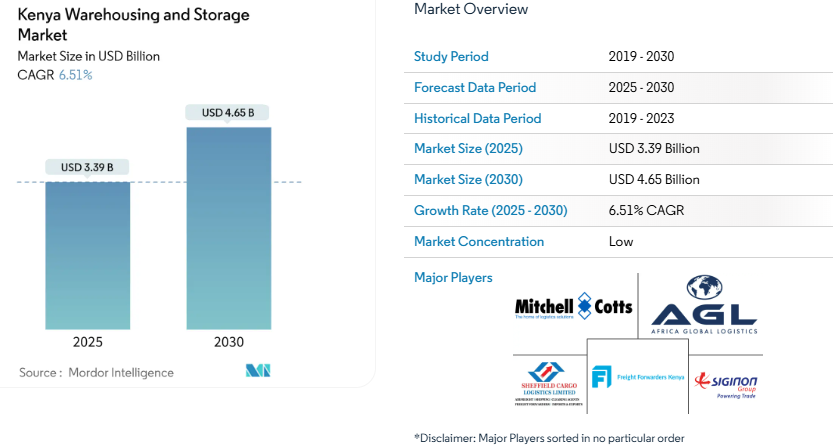

Warehousing Demand Continues Rising Around Nairobi

Despite ongoing cost pressure across the logistics sector, demand for modern warehousing space around Nairobi continued showing strong momentum in April.

Industrial zones surrounding Nairobi and key transport corridors are seeing growing interest from distributors, FMCG operators, retailers, and third-party logistics providers seeking strategically located storage and fulfilment facilities.

Part of the demand is being driven by changing inventory strategies. Following several years of supply-chain disruption globally, many businesses are maintaining higher stock buffers and placing greater emphasis on inventory availability and regional distribution readiness.

At the same time, customer expectations around fulfilment speed and delivery visibility continue pushing logistics providers toward more structured, technology-enabled warehouse operations.

The conversation around warehousing is also evolving beyond simple storage capacity. Increasingly, businesses are prioritizing operational efficiency, system integration, security, inventory accuracy, and scalability when selecting logistics partners.

As East Africa’s logistics sector matures, warehousing is steadily becoming a more strategic component of supply-chain design rather than simply a place to hold stock.